Importance of having at least two term insurance plans

The role of term insurance is simply undeniable for families, as it helped many families stay afloat and inspired them to lead a wholesome life even in the absence of the bread earner. Term insurance offers the utmost security with a high sum assured at an affordable premium. Though term insurance is still affordable, experts believe that one term insurance plan may not be sufficient to cover an individual’s needs at different stages of their life because of varying financial goals and needs. So, there are a plethora of reasons why a person should choose more than one term insurance policy during his lifetime.

If you are perplexed with the question “can I buy two-term insurance plans?” then take an expert’s opinion, and most experts suggest that you can purchase as many term plans as you need.

What is a term insurance plan?

A term plan offers financial protection to your family members at a reasonable rate. In case of the demise of the policyholder, the payment is made to the nominees. But there is no financial benefit if the policyholder is alive after the term.

When do you need more than one term life policy?

Can I have multiple term life insurance policies? Yes, you can have multiple term life insurance policies, and these policies are beneficial under the following scenarios.

- If one insurance provider rejects your claim: Sometimes, your beneficiaries’ claim may get rejected because of reasons like inadequate paperwork, unable to disclose the accurate health history, a poor claim settlement ratio of the insurance company, etc. If you have multiple term plans, you can overcome these situations and offer more protection to your family members.

- If your plan does not allow you to increase your cover with changing life stages: Most people purchase term plans at a young age (when they are not married or have children). But when they become a family man, they require a higher cover to satisfy their needs. If your existing plan doesn’t allow you to enhance your cover, you can go for another term plan.

- If you want better benefits: Not every term plan comes with rider benefits. If your existing plan doesn’t offer any rider benefits, then you can purchase another one.

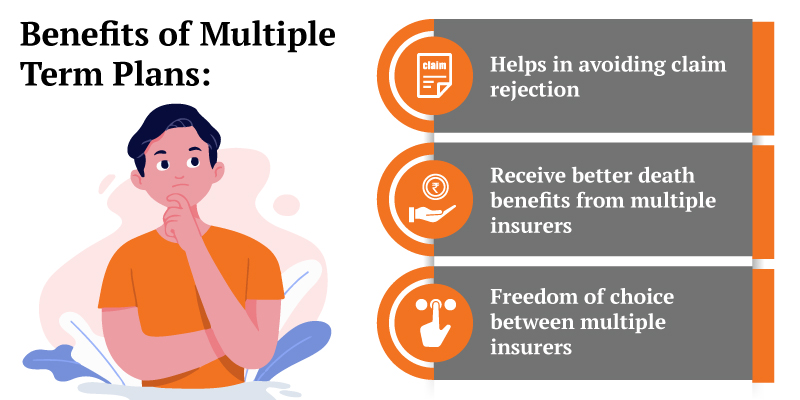

Top Benefits of two-term insurance plans

You may choose the same beneficiary or different nominees for both the term insurance plans. Let’s take a look at some prime benefits of two-term plans.

- Extra protection: By opting for more than one term insurance plan, you can offer extra protection to your family.

- Death benefit: Now, your nominees can get death benefits from more than one term policy.

- Avoid claim rejection: Since you have two-term plans, you don’t need to worry about claim rejection. In addition, if one company rejects your claim, you have another company to settle your claim. Thus, your family members will always stay protected.

- Claim settlement ratio: Different insurance companies have different claim settlement ratios. If the claim settlement ratio of an insurance provider is high, then the chances of your claim will also increase.

- Death claim: If there is a sudden demise of the policyholder before the end of the term plan, the nominee will receive a hefty amount that is called a death claim. The beneficiary will get payment as per the terms and conditions that are mentioned in the policy.

Before purchasing a second term insurance policy, you should provide the entire information about the first insurance policy to the second insurer. While purchasing a third policy, don’t forget to mention all the details of the first and second insurance policies with the third insurance provider. If you conceal any information, then your claims might be rejected.

Restrictions

Certain restrictions are there if you want to possess more than one term plan.

- You need to ensure that the sum assured of all the insurance policies never goes beyond the Human Life Value.

- The insurance provider is responsible for the risk assessment. Once your proposal is submitted, it will go through the underwriting process. The insurer will evaluate different types of health-related risks before deciding your premium and the sum assured.

- Your term insurance is dependent on your annual income and the existing life cover.

Claiming multiple insurance policies

Can I claim two-term insurance policies? Let’s dig deeper.

Before claiming your multiple policies, you should finish all imperative information about the insurers’ term insurance plans. Most insurance companies abide by the guidelines set by the IRDAI (Insurance Regulatory Development Authority of India).

In case of any issue in the claiming policy, a ticket will be generated with the respective insurance provider. If your insurance company doesn’t respond, then IRDAI will take care of everything.

How do you apply for multiple insurance plans?

- Approach the right company: After comparing various insurance plans from multiple companies, choose the right company that offers the best insurance plan.

- Medical Tests: You only need to go for the medical examination once, and then, you can share those reports and information with all insurance providers.

- Insurability: The insurance company will decide the sum assured to the beneficiary. You should provide all necessary documents to your insurance company. If you are mentioning your close family members like father, mother, son, or daughter as nominees, your application will be processed easily and quickly.

- Evaluate your insurance needs: Evaluate your insurance needs based on changing income and familial responsibilities. You should opt for a second insurance plan if it doesn’t provide any financial stress to you.

- Purchasing at a young age: Always purchase a term insurance plan at a young age when the premium is low. Hence, you can comfortably pay premiums without stretching your financial condition.

- Reviews: Choose a term plan after going through the reviews of the experts. Thus, you can choose the best term plan for you. To enhance your benefits, you may choose riders for an insurance policy.

“Can you have more than one term life insurance policy?” Now, you have sufficient information for this question. Sometimes, it could be an uphill task for you to manage multiple policies as you need to pay add-on premiums. However, you can adopt multiple policies if the benefits surpass the difficulties in managing term plans.